Back in 2003, the Treasury began selling 5-year Treasury Inflation Protected Securities, or TIPS. (Longer maturities were available starting in 1997.) What happens is that the government pays a fixed coupon rate, but the principal is adjusted based on increases in the Consumer Price Index (CPI). Thus, TIPS yields are one of the closest things you can get to observing the real interest rate; it measures what lenders need to be offered to part with their money for a period of time, over and above the fall in the purchasing power of their money.

TIPS are really neat because, in theory, they should allow you to back out the market’s expected rate of inflation (subject to a million caveats, as everything in mathematical finance is). The nominal yields on Treasurys (and yes, that’s how The Man spells it, not Treasuries) incorporate both the real yield and expected inflation, and so Nominal minus TIPS (for comparable maturities) should give the average expected inflation rate during the life of the bonds. (Again, I want to stress that this is a simplification. For example, regular Treasurys are more liquid than TIPS, and so you would expect the former to have a slightly lower yield for this reason.)

Anyway, a lot of people are currently trying to calm investors by pointing to the bond market. “Look,” they might say, “the monthly averages show that in August, five-year nominal Treasurys were yielding just under 2 percentage points more than TIPS. So that means the market expects average inflation of only 2 percent per year, over the next five years. Do you Chicken Littles think you know more than all the world’s bond traders?”

OK I think one would have to be INSANE to predict average (price) inflation of only 2 percent over the next five years. It will be much higher than that. (Note that I am talking about the overall CPI for urban consumers, not the “core inflation” that deviously removes food and energy prices.) So what gives? Well, one thing is that–as noted in the parenthetical remarks above–there might be a liquidity premium placed on nominal Treasurys, even versus TIPS. Another is that nominal Treasurys are safer, especially as things get crazier and crazier.

It’s not so much that the government will default on TIPS, but rather that they might stop indexing them for inflation. Another possibility for why the market is apparently underestimating future inflation is that the bond traders know full well how full of BS the BLS is, and so the “Inflation Protected” securities aren’t really fully covering their owners. For example, if an investor expects actual price inflation of 5 percent per year, and he requires a real yield of 1 percent, then in theory he should buy a TIPS yielding 1 percent. But what if he knows that the BLS will understate the true inflation rate, and instead announce annual CPI increases of only (say) 3 percent per year, in contrast to the true inflation rate of 5 percent? In that case, the investor who requires a real yield of 1 percent will insist on a TIPS yield of 3 percent. Thus, naive analysts who trust the BLS (or who think bond traders do) would say, “Sweet! The bond market is anticipating strong economic growth, with expected real yields of 3 percent!” Note that this same bond trader–who remember expects actual inflation of 5 percent and requires a real yield of 1 percent–would buy regular Treasurys yielding 6 percent. So by our method of simple subtraction, we would erroneously conclude that this bond trader expects 6 – 3 = 3 percent inflation, when we know he really anticipates 5 percent. The difference is how much the bond trader thinks the government will understate inflation.

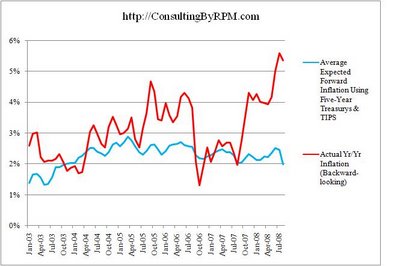

Finally, I have done some empirical analysis to see how the (Nominal-TIPS) technique has done so far. Now unfortunately, you can’t do a true test, because the 5-year TIPS have only been around for a little over five years. However, even so I think the chart below (click to enlarge) is very instructive. It contrasts the monthly “expected future five-year inflation rate” (based on nominal minus TIPS yields) versus the monthly actual, backward-looking year-over-year increase in the CPI. I think it should be obvious that the bond market is not currently forecasting 2% inflation over the next five years.

Robert P. Murphy is an economist with the Institute for Energy Research and author of The Politically Incorrect Guide to Capitalism. He writes an infromative blog called Free Advice and you can email him at [email protected]

TIPS Have Underforecasted Inflation

Robert P. Murphy

Back in 2003, the Treasury began selling 5-year Treasury Inflation Protected Securities, or TIPS. (Longer maturities were available starting in 1997.) What happens is that the government pays a fixed coupon rate, but the principal is adjusted based on increases in the Consumer Price Index (CPI). Thus, TIPS yields are one of the closest things you can get to observing the real interest rate; it measures what lenders need to be offered to part with their money for a period of time, over and above the fall in the purchasing power of their money.

TIPS are really neat because, in theory, they should allow you to back out the market’s expected rate of inflation (subject to a million caveats, as everything in mathematical finance is). The nominal yields on Treasurys (and yes, that’s how The Man spells it, not Treasuries) incorporate both the real yield and expected inflation, and so Nominal minus TIPS (for comparable maturities) should give the average expected inflation rate during the life of the bonds. (Again, I want to stress that this is a simplification. For example, regular Treasurys are more liquid than TIPS, and so you would expect the former to have a slightly lower yield for this reason.)

Anyway, a lot of people are currently trying to calm investors by pointing to the bond market. “Look,” they might say, “the monthly averages show that in August, five-year nominal Treasurys were yielding just under 2 percentage points more than TIPS. So that means the market expects average inflation of only 2 percent per year, over the next five years. Do you Chicken Littles think you know more than all the world’s bond traders?”

OK I think one would have to be INSANE to predict average (price) inflation of only 2 percent over the next five years. It will be much higher than that. (Note that I am talking about the overall CPI for urban consumers, not the “core inflation” that deviously removes food and energy prices.) So what gives? Well, one thing is that–as noted in the parenthetical remarks above–there might be a liquidity premium placed on nominal Treasurys, even versus TIPS. Another is that nominal Treasurys are safer, especially as things get crazier and crazier.

It’s not so much that the government will default on TIPS, but rather that they might stop indexing them for inflation. Another possibility for why the market is apparently underestimating future inflation is that the bond traders know full well how full of BS the BLS is, and so the “Inflation Protected” securities aren’t really fully covering their owners. For example, if an investor expects actual price inflation of 5 percent per year, and he requires a real yield of 1 percent, then in theory he should buy a TIPS yielding 1 percent. But what if he knows that the BLS will understate the true inflation rate, and instead announce annual CPI increases of only (say) 3 percent per year, in contrast to the true inflation rate of 5 percent? In that case, the investor who requires a real yield of 1 percent will insist on a TIPS yield of 3 percent. Thus, naive analysts who trust the BLS (or who think bond traders do) would say, “Sweet! The bond market is anticipating strong economic growth, with expected real yields of 3 percent!” Note that this same bond trader–who remember expects actual inflation of 5 percent and requires a real yield of 1 percent–would buy regular Treasurys yielding 6 percent. So by our method of simple subtraction, we would erroneously conclude that this bond trader expects 6 – 3 = 3 percent inflation, when we know he really anticipates 5 percent. The difference is how much the bond trader thinks the government will understate inflation.

Finally, I have done some empirical analysis to see how the (Nominal-TIPS) technique has done so far. Now unfortunately, you can’t do a true test, because the 5-year TIPS have only been around for a little over five years. However, even so I think the chart below (click to enlarge) is very instructive. It contrasts the monthly “expected future five-year inflation rate” (based on nominal minus TIPS yields) versus the monthly actual, backward-looking year-over-year increase in the CPI. I think it should be obvious that the bond market is not currently forecasting 2% inflation over the next five years.

Robert P. Murphy is an economist with the Institute for Energy Research and author of The Politically Incorrect Guide to Capitalism. He writes an infromative blog called Free Advice and you can email him at [email protected]

Nothing contained in this blog is to be construed as necessarily reflecting the views of the Pacific Research Institute or as an attempt to thwart or aid the passage of any legislation.